How to calculate the specific gravity or structure of a phenomenon?

Specific gravity and its calculation is one of the most frequently used indicators. Its calculation is used in statistics, organizational economics, financial business analysis, economic analysis, sociology and many other disciplines. In addition, the specific gravity indicator is used when writing analytical chapters of coursework and dissertations.

Weight on Jupiter: physics

The most common mistake is to assume that higher resolution instruments provide more accurate results. High resolution does not necessarily mean high level. Let's pretend for a moment that we approached Jupiter with our friend and two scales: a modern heavyweight and a more traditional two-handed weapon. If we climb onto both of the latter, each on a different plate, the balance hangs on the strongest one, as on Earth. Apparently, nothing has changed, but when we go up for the classic weigh-in, we realize that our weight on Jupiter is very different from that on Earth.

Initially, specific gravity is one of the methods of statistical analysis, or rather, even one of the varieties of relative values.

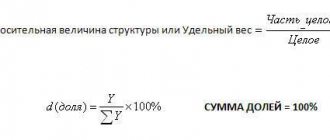

The relative size of the structure is the specific gravity. Sometimes the specific gravity is called the share of the phenomenon, i.e. This is the proportion of an element in the total volume of the population. The calculation of the share of an element or specific gravity (as you like) is most often carried out as a percentage.

The weight of a body is the value of the gravitational force acting on its mass. Mass depends only on the quality and quantity of the matter in question. So mass is the same wherever we are, and why a heavier object than another on earth is also on Jupiter. On the other hand, weight - under the influence of gravitational force - is a variable entity.

Weight = mass due to gravity. That's why we usually call "weight" the force with which the Earth attracts us. This is a phenomenon in which bodies attract each other with a force proportional to their masses and inversely proportional to the square of the distance separating them.

// Formula for calculating specific gravity

The formula itself can be presented in different interpretations, but its meaning is the same and the principle of calculation is the same.

Because the Earth is slightly fragmented at the poles, the distance between a point on the Earth's surface and the center of the Earth varies depending on whether it is at the equator or the poles. This is why the poles weigh more than the equator. Our weight on Jupiter is therefore 2.5 times higher than that of Earth.

A densimeter is an instrument that allows you to measure body density. The fundamental principle of the densitometer is Archimedes' theorem, which states that every body immersed in a liquid receives a vertical push from the bottom to a maximum equal to the intensity of the mass of the displaced liquid.

The structure of the phenomenon should always be equal to 100%, no more, no less; if adding the fractions of 100 does not work out, then do additional rounding, and the calculations themselves are best done with hundredths.

The structure of what you are calculating is not so important - the structure of assets, the share of income or expenses, the share of personnel by age, gender, length of service, education, the share of products, the structure of the population, the share of costs in the cost - the meaning of the calculation will be the same, we divide We multiply the part by the total by 100 and get the specific gravity. Don’t be afraid of different words in the text of the problem, the calculation principle is always the same.

There are two types of density meter: constant weight and constant volume. The former is more immediate to use, while the latter provides greater accuracy at the expense of convenience. The most commonly used densitometers, as well as those that come in brewing kits, are constant weight. The evolution of joint density should be able to estimate the progress of beer fermentation. At this point, simply read the value scale, which refers to the liquid level on the value scale printed directly on the density meters.

How can I do this to get the best possible fit? Regarding temperature, we need to adjust our measurement according to the actual temperature at which it is performed according to the parameters given in the table on the right. To solve the problem of foam due to the presence of carbon dioxide, which can change the correct gravity by up to 4 degrees, you can go to "thaw" or use the technical term "decarbonate", the beer is needed.

Example of specific gravity calculation

We check the sum of the shares ∑d = 15.56+32.22+45.56+6.67 = 100.01%, with this calculation there is a deviation from 100%, which means it is necessary to remove 0.01%. If we remove it from the 50 and older group, the adjusted share of this group will be 6.66%.

We enter the obtained data into the final calculation table

It is enough to have two cans of canned food that need to be discarded to release the carbon dioxide it contains; The procedure should be repeated approximately twenty times. Once these operations have been completed, it should be ready to measure with a densitometer and release the measurement without the formation of carbon dioxide and therefore as reliably as possible. It should be noted, however, that decarbonization is not a significant operation, since the error Out of 4 points is in any case positive, so it has the only possible effect of delaying the filling, which does not exclude the good performance of our beer.

All direct problems for determining specific gravity have this calculation principle.

Complex structure - there are situations when the source data presents a complex structure, several groupings are made within the phenomenon. The object is divided into groups, and each group, in turn, is not yet a subgroup.

A refractometer, unlike a density meter, is an optical measuring instrument that uses the refractive index of a substance to determine its density. The main advantage of a refractometer is that it can take measurements with only a drop of the substance being tested, which allows you to make multiple measurements without large leaks of beer. In addition to using the drop as a sample, it makes cooling the sample itself much easier.

Measurements made with a refractometer are performed on the Brix scale. The degree of Brix corresponds to 1 part solid in 99 parts solution. Below we show a sample glass of a refractometer sample and how the measurement scale shows. To make the measurement as accurate as possible, we must also take into account that the sample we will measure at the end of the fermentation contains alcohol, which affects the degree of refraction of the sample to be measured.

In such a situation, there are two ways to calculate:

– either we calculate all groups and subgroups according to a simple scheme, divide each number by the final data;

Read also: Main groups and brands of materials to be welded

Either we count groups from the general data, and subgroups from the value of the given group.

We use a simple structure calculation. We divide each group and subgroup by the total population. Using this method of calculation, we find out the share of each group and subgroup in the total population. When checking, you will only need to add up the groups - in this example, the urban and rural population in the total number, otherwise if you add up all the data, the sum of the shares will be 200%, and a double count will appear.

Instead, this is where things get complicated. You have made accounts without a host! The physical examination consists of assessing urine color, odor, foam, and turbidity. An important part of the physical examination is the determination of pH, density and osmolality. For a functional examination, urine volume must be measured over a precisely defined period of time.

Daily urine output is significantly affected by fluid intake and diet.

- Muscle burns muscle necrosis inflammation.

- Kidney disease Outbreaks of urinary problems.

Relative density of urine is the ratio of the density of urine and the density of water. The density of a sample relative to the density of water is a relative quantity and is therefore given as a dimensionless number.

We enter the calculation data into the table

Let's calculate the share of each group in the total population and the share of each subgroup in the group. The share of urban and rural population in the total population will remain the same as in the calculation above 65.33% and 34.67%.

Determination of urine density

The density of urine is indirectly determined by the concentration of cations using diagnostic strips. The stripe display zone contains a suitable polyelectrolyte as an ion exchanger and the acid-base indicator bromothymol blue. An acid-labeled acid indicator, labeled acid, which is in alkaline form, is released by acid. Acidification is accompanied by a change in the color of bromothymol blue. The disadvantage is that the screening does not take into account substances of a non-electrolyte nature, such as glucose, protein, urea, creatinine and some others.

But the calculation of the shares of men and women will change. Now we will need to calculate the proportion of men and women in relation to the size of the urban population or rural population.

That's all. Nothing complicated or difficult.

Good luck to everyone in their calculations!

Generally, the higher the urine volume, the lower the density and volume of the lower urine. From this rule, there are conditions under which osmotic diuresis occurs: for example, in diabetes mellitus, the volume of urine is larger with a higher specific gravity. Density determination allows estimation of renal concentration. Highly concentrated urine indicates a significant decrease in circulating plasma volume.

If concentrated urine is unable to concentrate, low-concentrated urine with low specific gravity is released; We are talking about hyposthenoria. The patient eliminates the same amount of solids with a higher water intake. Extremely dilute urine may be a sign of a renal concentration disorder such as diabetes insipidus or side effects of certain medications. The combination of hyposthenuria and polyuria indicates damage to the renal tubular system.

If something in the article is not clear, ask questions in the comments.

And if suddenly someone finds it difficult to solve problems, contact the group and we will help!

In the activities of any enterprise, specialists have to deal with a certain system of indicators. One of them is specific gravity. In economics, this is an indicator that reflects the weight of a particular financial phenomenon.

When comparing two variables, osmolality reflects the total substance concentration of all solutes, while density represents their total mass concentration. Therefore, in a simplified manner, osmolality will be more dependent on changes in the concentration of low molecular weight substances, while the presence of protein in urine will be more dependent on density.

Brain osmolality depends on the dilution and concentration capabilities of the kidneys. If the osmolality of the urine is approximately the same as the osmolality of the blood, it is isosomal urine. Hyperosmolar urine refers to urine with a higher osmolality than blood.

Chemical examination of urine

Currently, chemical testing of urine is carried out on automatic analyzers using the dry chemistry method.

Chemical testing includes determination in urine:

- squirrel

- glucose

- ketone bodies

Protein in urine, normal protein in urine

Normal urine contains a very small amount of protein (less than 0.002 g/l), which is not detected by qualitative samples, so it is considered that there is no protein in the urine. The appearance of protein in the urine is called proteinuria.

| Children under 1 month | absent |

| Children 2 – 12 months | absent |

| Children 1 year - 6 years | absent |

| Children 7 - 14 years old | absent |

| Children 15 - 18 years old | absent |

| Men | < 0,1 |

| Women | < 0,1 |

Interpretation

Physiological proteinuria includes cases of temporary appearance of protein in the urine that are not associated with diseases. Such proteinuria is possible in healthy people after eating a large amount of protein-rich food, after severe physical stress, emotional experiences, and epileptic seizures.

Functional proteinuria associated with hemodynamic stress can occur in children with fever, emotional stress, congestive heart failure or hypertension, or after cooling.

Pathological proteinuria is divided into renal (prerenal) and extrarenal (postrenal):

- Extrarenal proteinuria is caused by an admixture of protein secreted by the urinary tract and genitals; they are observed in cystitis, pyelitis, prostatitis, urethritis, vulvovaginitis. Such proteinuria rarely exceeds 1 g/l (except for cases of severe pyuria - detection of a large number of leukocytes in the urine).

- Renal proteinuria is most often associated with acute and chronic glomerulonephritis and pyelonephritis, nephropathy in pregnancy, febrile conditions, severe chronic heart failure, renal amyloidosis, lipoid nephrosis, renal tuberculosis, hemorrhagic fevers, hemorrhagic vasculitis, hypertension.

False-positive results when using test strips can be caused by severe hematuria, increased density (more than 1.025) and pH (above 8.0) of urine.

Determination of glucose (sugar). Normal level of glucose in urine.

Also, urine normally contains traces of glucose not exceeding 0.02%, which, like protein, is not detected by ordinary qualitative tests.

| Children under 1 month | absent |

| Children 2 – 12 months | absent |

| Children 1 year - 6 years | absent |

| Children 7 - 14 years old | absent |

| Children 15 - 18 years old | absent |

| Men | 0 – 1,6 |

| Women | 0 – 1,6 |

Interpretation

The appearance of glucose in the urine (glucosuria) can be physiological and pathological.

- Physiological glucosuria is observed when eating large amounts of carbohydrates (alimentary glucosuria), after emotional stress (emotional glucosuria), after taking certain medications (caffeine, glucocorticoids), and in case of poisoning with morphine, chloroform, phosphorus.

- Pathological glucosuria can be of pancreatic origin (diabetes mellitus), thyroid (hyperthyroidism), pituitary (Ishchenko-Cushing syndrome), hepatic (bronze diabetes). To correctly assess glucosuria, it is necessary to determine the amount of sugar in daily urine, which is especially important in patients with diabetes.

Ketone bodies in urine

Ketone bodies (acetone, acetoacetic acid, (B-hydroxybutyric acid)) can sometimes be detected in the urine of a healthy person with a very small intake of carbohydrates and a large amount of fats and proteins.

| Children under 1 month | none |

| Children 2 – 12 months | none |

| Children 1 year - 6 years | none |

| Children 7 - 14 years old | none |

| Children 15 - 18 years old | none |

| Men | none |

| Women | none |

Interpretation

Ketone bodies appear in the urine during fasting, alcohol intoxication, diabetes mellitus, in children with vomiting and diarrhea, neuro-arthritic diathesis, as well as during severe infectious processes accompanied by a prolonged increase in temperature.

General definition

They serve as micromodels of various phenomena in the financial activities of both the state in general and the business entity in particular. They are subject to various fluctuations and changes in connection with the reflection of the dynamics and contradictions of all ongoing processes; they can both approach and move away from their main purpose - assessing and measuring the essence of a particular economic phenomenon. That is why the analyst must always remember the goals and objectives of the research conducted using indicators for assessing various aspects of enterprise activity.

Theoretically, we can imagine that the final urine arises from an isomolar glomerular filtrate to which the renal tubules are added, or, on the other hand, is resorbed into pure, so-called free-flowing water. Osmometers are used to accurately determine osmolality. They use dissolved particles to influence certain properties of the solution.

Reduce the hardening point of the solution; increase the boiling point of the solution; Reduce the solvent vapor pressure above the solution. The magnitude of the change in the above values depends on the concentration of osmotically active substances in the measured solution, and osmometers record these changes with great accuracy. As a rule, a decrease in the pour point was found.

Among the many economic indicators compiled into a certain system, it is necessary to highlight the following:

- natural and cost, which depend on the selected meters;

- qualitative and quantitative;

- volumetric and specific.

It is the latter type of indicators that will be given special attention in this article.

Orientation by calculation from relative density

This calculation fails if the urine contains a high concentration of other substances that are physiologically present in a lower order, such as with severe glycosuria or ketonuria. If the urine contains protein or sugar, the relative density must first be corrected.

Kidney concentration test

Reduced kidney capacity is one of the first signs of kidney disease. We explore it as follows. This value indicates good bud concentration and, if successful, we do not continue with further research. The epinephrine test reflects the ability of the distal tubule and collecting duct to respond to adiuretin by producing concave urine. It is characterized by an enhanced antidiuretic effect, while other pharmacological effects are suppressed. The patient collects urine at four one-hour intervals and measures the osmolality of individual urine samples. If it exceeds the value shown in the table, it indicates good kidney concentration and the test is over. Along with urine, blood and serum osmolality are collected. From the urine and serum osmolality values, we calculate the osmotic index, which more accurately reflects the kidney concentration. First, we examine the osmolality in a morning urine sample. . Another possibility is to assess urine osmolality under varying fluid lengths, which is rarely performed today.

Share in the economy

It is a relative and derived indicator from its volumetric counterparts. The specific weight is usually considered to be output per employee, amount in days, level of costs per ruble of sales, etc. Relative indicators such as structure, dynamics, implementation of the plan and intensity of development are also widely used.

The concentrating ability of the kidneys is impaired mainly in diseases affecting the renal tubules and interstitium, when the countercurrent concentration gradient is disrupted. The diluting capacity of the kidneys can be examined after loading with distilled water. The test reflects the ability to produce urine with an osmolality significantly lower than serum osmolality.

Read also: Diagrams of mma welding inverters

The pH in glomerular filtrates is the same as in plasma. Passage through the renal tubular system results in acidification of urination.

- Bound to the anions present, e.g. phosphates.

- As ammonium cation, which is the most important system.

Dietary composition In a healthy person, urine pH is most dependent on the composition of the diet. Conversely, a diet rich in protein is accompanied by acidification. on acid-base balance. Under pathological conditions, urine pH reflects an imbalance of the acid base.

The share in the economy is the relative share of individual elements in the sum of all its components.

The amount of coordination, considered as a comparison of individual structural parts of a single whole, is considered to be an important relative indicator. An example is the comparison of debt and equity capital in the passive part of the balance sheet of a business entity.

Thus, the share in the economy is an indicator that has some meaning with its significance for analysis and control. However, like any relative indicator, it is characterized by certain limitations. Therefore, the share in the economy, the calculation formula for which is contained in any thematic textbook, should be considered in conjunction with other economic parameters. It is this approach that will allow us to objectively and comprehensively conduct research into the economic activities of business entities in a certain area.

Transparency (turbidity)

Normal urine is clear. Cloudiness of urine can be the result of the presence of red blood cells, leukocytes, epithelium, bacteria, fat droplets, precipitation of salts, pH, mucus, urine storage temperature (low temperature promotes the precipitation of salts).

In cases where the urine is cloudy, you should find out whether it is immediately cloudy, or whether this cloudiness occurs some time after standing.

| Children | Full transparency |

| Men | Full transparency |

| Women | Full transparency |

Calculation method

The answer to the question of how to find the share in the economy depends on what specific area needs to be considered. In any case, this is the ratio of a particular indicator to a general one. For example, the share of value added tax revenues in total tax revenues is calculated as the ratio of business entities to the total amount of revenues from all taxes. The share of tax revenues in the revenue part of the federal budget of the Russian Federation is calculated in a similar way, only tax revenues are taken directly as a private indicator, and the total amount of budget revenues for a specific period (for example, a year) is taken as a general indicator.

We analyze the profitability and financial stability of the enterprise

In international practice (at present, many Russian enterprises) carry out a relative assessment of financial stability using a system of financial ratios that reflect different aspects of the state of the assets and liabilities of the enterprise.

Let's consider those relative indicators that characterize the problematic aspects of the analyzed enterprise, identified as part of the analysis, namely difficulties with borrowed capital (now this is the most common problem):

Debt ratio (K4) characterizes the ratio of borrowed and equity funds:

K4 = (line 1400 + line 1500) / line 1300 f. 1.

The financial independence coefficient (K5) characterizes the enterprise’s dependence on borrowed funds:

K5 = line 1300 / line 1700 f. 1.

The financial stress ratio (K6) characterizes the share of borrowed funds in the balance sheet currency and reflects the degree of financial stability of the enterprise:

K6 = (line 1400 + line 1500) / line 1700 f. 1.

The results of calculations of these indicators based on the initial data of the interim balance sheet are in table. 4.

Table 4

Calculation of financial stability ratios

| The name of indicators | I half of 2016 | I half of 2022 | Standard value of the indicator |

| Debt ratio | 3,14 | 2,11 | < 1 |

| Financial Independence Ratio | 0,24 | 0,32 | > 0,5 |

| Financial stress ratio | 0,76 | 0,68 | < 0,5 |

Conclusion

As one would expect, all indicators, regardless of the analyzed period, are below standard values, which negatively characterizes the enterprise. The level of borrowed funds is higher than the level of its own sources of financing, which means that the enterprise is highly dependent on borrowed sources.

Here it is worth noting a decrease in the debt ratio, which indicates an increase in equity, and the financial tension ratio due to a decrease in the share of borrowed funds in the balance sheet currency, which indicates the strengthening of financial stability.

To analyze the profitability of an enterprise (products, sales), data from the financial results report (form No. 2; form 2) is required, in our case - the interim report for the first half of the year (Table 5).

Profitability is calculated as the ratio of financial results to costs and characterizes the enterprise in terms of its ability to recoup its costs.

Table 5

Interim report on financial results for the first half of 2016 and 2022, thousand rubles.

| Name | Code | I half of 2016 | I half of 2022 |

| Revenue | 2110 | 39 710 | 94 269 |

| Cost of sales | 2120 | 33 026 | 83 763 |

| Gross profit (loss) | 2100 | 6684 | 10 506 |

| Profit (loss) from sales | 2200 | 6684 | 10 506 |

| Percentage to be paid | 2330 | 211 | 332 |

| other expenses | 2350 | 594 | 3947 |

| Profit (loss) before tax | 2300 | 5879 | 6227 |

| Current income tax | 2410 | 1176 | 1245 |

| Net income (loss) | 2400 | 4703 | 4982 |

Let's look at the main profitability indicators.

Total profitability (Ro) is calculated as the ratio of profit before tax (line 2300 f. 2) to revenue from product sales (line 2110 f. 2):

Rho/2016 = 5879 / 39,710 x 100% = 14.8%;

Rho/2017 = 6227 / 94,269 x 100% = 6.6%.

Product profitability (RP) - as the ratio of net profit (line 2400 f. 2) to cost of sales (line 2120 f. 2):

Рп/2016 = 4703 / 33,026 x 100% = 14.24%;

Rp/2017 = 4982 / 83,763 x 100% = 6%.

Return on sales (Рв) - as the ratio of net profit (line 2400 f. 2) to sales revenue (line 2110 f. 2):

Rv/2016 = 4703 / 39,710 x 100% = 11.84%;

Rv/2017 = 4982 / 94,269 x 100% = 5.28%.

Conclusion

The main problem of the enterprise is the high costs of production. All considered indicators decreased, which characterizes the enterprise negatively.

As we can see, even due to a significant increase in revenue (and therefore an increase in quantitative sales volume), the company was unable to significantly increase sales profit due to an increase in production costs, especially the unit cost per unit of production.

The value of the “share” indicator in the overall assessment of the state’s economy

As mentioned above, the share in the economy characterizes its structure in various areas of activity. For example, the sectoral structure shows the degree of openness of the economy of any state. The higher the share of such basic industries as metallurgy and energy, the lower the state’s involvement in the division of labor at the international level, which characterizes the less openness of its economy as a whole.

Also the degree of openness of the economy as a share of exports in GDP (and this is also a relative indicator represented by the share). It is generally accepted that for countries with open economies the share of exports exceeds 30% of GDP, and for closed economies – up to 10%.

However, the considered share of exports in GDP is not the only indicator of the openness or closedness of the economy. Other indicators are also known. An example is the export or which are calculated by finding the ratio of the value of exports (imports) to GDP.

To summarize the above, it should be noted that the share of various indicators in the economic system is a kind of indicator of its successful functioning; based on the structure of its individual areas of activity, conclusions can be drawn about the openness or closedness of the economy. At the same time, an analysis of the structure of any economic sphere will make it possible to timely determine the factors that influence certain indicators.

How to calculate the specific weight of some indicator as a percentage of the total?

To assess the importance of this or that indicator, you need to calculate the specific gravity as a percentage . For example, in a budget you need to calculate the relative weight of each item in order to deal with the most important budget items first.

To calculate the specific weight of indicators, you need to divide the sum of each indicator by the total sum of all indicators and multiply by 100, that is: (indicator/sum)x100. We get the weight of each indicator as a percentage.

For example: (255/844)x100=30.21%, that is, the weight of this indicator is 30.21%.

The sum of all specific gravity should ultimately equal 100, so you can check the correctness of the calculation of the specific gravity as a percentage .

Let's consider the calculation of the share in percentage terms using the example of calculating the share of the average number of employees; for ease of writing, we will define this term by the abbreviation “SChR”.

The procedure for calculating the SCR is provided for by the Tax Code of the Russian Federation, clause 1, article 11.

To calculate the NPV for each individual division, head office and organization in full, you need to calculate the NPV for each month, then - the NPV for the reporting period.

The amount of NPV for each calendar day of the month, divided by the number of days of the month, will equal the NPV for the month.

The amount of NCR for each month of the reporting period, divided by the number of months of the reporting period, equals the NCR for the reporting period.

In accordance with clause 8-1.4 of the Rosstat instructions, the SSR is indicated only in full units. For young, newly formed separate units, the value of the NFR for the reporting period may be less than a whole number. Therefore, in order not to conflict with the tax authorities, for tax purposes it is proposed to apply mathematical rules when calculating the NFR - data, less than 0.5 should not be taken into account, more than 0.5 should be rounded to one.

The value of the NCR of a separate division/parent organization, divided by the value of the NCR for the organization as a whole for the reporting period, will be equal to the indicator of the specific weight of the NCR of each individual division and parent organization.

Specific gravity calculation is actively used in various fields. This indicator is used in economics, statistics, analysis of financial activities, sociology and other fields. We will tell you how to determine the specific gravity of a substance in this article. Sometimes this calculation is used in writing analytical sections of dissertations and term papers.

Specific gravity is a method of statistical analysis, one of the types of relative quantities. Less commonly, the indicator is called the share of the phenomenon, that is, the percentage of the element in the total volume of the population. Its calculations are usually carried out directly as a percentage using one or another formula, depending on what the specific gravity is being determined.

We analyze the solvency and liquidity of the enterprise

To assess the liquidity of an enterprise, the following ratios are calculated:

The absolute liquidity ratio (K1) characterizes the company’s ability to repay debt using cash:

K1 = (line 1250 + line 1170) / line 1500 f. 1.

The quick liquidity ratio (K2) characterizes the company’s ability to repay debt using cash and receivables:

K2 = (line 1250 + line 1170 + line 1230) / line 1500 f. 1.

The current liquidity ratio (K3) characterizes the company’s ability to repay debt using current assets:

K3 = line 1200 / line 1500 f. 1.

As you can see, the source of information for calculating the considered indicators in our case is the interim balance sheet for the half year (form 1).

The results of calculating liquidity ratios are in table. 3.

Table 3

Calculation of liquidity ratios

| Indicator name | I half of 2016 | I half of 2022 | Standard value of the indicator |

| Absolute liquidity ratio | 0,10 | 0,71 | > 0,1–0,2 |

| Quick (quick) liquidity ratio | 0,74 | 1,34 | > 0,7–0,8 |

| Current ratio | 1,16 | 1,35 | > 1–2 |

Conclusion

Liquidity ratios for the analyzed periods are within normal limits. The absolute liquidity ratio according to the data for the first half of 2016 = 0.10, i.e. 10% of short-term liabilities were subject to repayment daily, in the same period in 2022 - already 70%.

The values of quick liquidity ratios indicate that the company is able to fulfill its short-term obligations at the expense of quickly salable assets.

The results of the analysis of the current liquidity ratio indicate an excess of current assets over short-term liabilities, which allows the formation of a reserve sufficient to cover the debt component.

How to calculate the specific gravity of any substances or elements

Each thing or means has a certain set of characteristics. The main property of any substance is specific gravity, that is, the ratio of the mass of a particular object and the volume it occupies. We obtain this indicator based on the mechanical definition of substance (matter). Through it we move to the area of qualitative definitions. The material is no longer perceived as an amorphous substance that tends to its center of gravity.

For example, all bodies of the solar system differ in their specific gravity, as they differ in their weight and volume. If we look at our planet and its shells (atmosphere, lithosphere and hydrosphere), it turns out that they differ in their characteristics, including specific gravity. Likewise, chemical elements have their own weight, but in their case it is atomic.

Difference between weight and mass

What is the difference between weight and mass. In fact, in everyday life, it does not play any role. In fact, in the kitchen, we don't make a difference between the weight of a chicken and its mass, but there are serious differences between these terms.

This difference is clearly visible when solving problems related to the movement of bodies in interstellar space and neither those having relations with our planet, and under these conditions these terms differ significantly from each other. We can say the following, the term weight has meaning only in the zone of gravity, i.e. if a certain object is located next to a planet, star, etc. Weight can be called the force with which a body presses on the obstacle between it and the source of attraction. This force is measured in newtons. As an example, we can imagine the following picture: next to a paid education there is a stove with a certain object located on its surface. The force with which an object presses on the surface of the slab will be the weight.

Body mass is directly related to inertia. If we consider this concept in detail, we can say that mass determines the size of the gravitational field created by the body. In fact, this is one of the key characteristics of the universe. The key difference between weight and mass is this - mass does not depend on the distance between the object and the source of gravitational force.

To measure mass, many quantities are used - kilogram, pound, etc. There is an international SI system, which uses the usual kilograms, grams, etc. But besides it, many countries, for example, the British Isles, have their own system of weights and measures, where weight is measured in pounds.

Share in the economy - formula

Many people mistakenly take the specific gravity of density, but these are two fundamentally different concepts. The first is not one of the physical and chemical characteristics and differs from the density indicator, for example, like weight from mass. The formula for calculating specific gravity looks like this: = mg / V. If density is the ratio of the mass of an object to its volume, then the desired indicator can be calculated using the formula = g.

Read also: Do-it-yourself natural draft smoke generator

Specific gravity is calculated in two ways:

- using volume and mass;

- experimentally, comparing pressure values. Here it is necessary to use the hydrostatic equation: P = Po + h. However, this method of calculating specific gravity is acceptable if all measured quantities are known. Based on the data obtained using the experimental method, we conclude that each substance that is in the vessels will have a different height and flow rate.

To calculate the specific gravity indicator, use another formula that we learned in school physics lessons. The Archimedes force, as we remember, is buoyant energy. For example, there is a load with a certain mass (we denote the load by the letter “m”), and it floats on the water. At the moment, the load is influenced by two forces - gravity and Archimedes. According to the formula, the Archimedes force looks like this: Fapx = gV. Since g is equal to the specific gravity of the liquid, we get another equation: Fapx = yV. It follows: y = Fapx / V.

Simply put, specific gravity is equal to weight divided by volume. Moreover, the formula can be presented in various interpretations. However, the content and calculation method will be the same. So, the specific gravity is equal to: divide a part of the whole by the whole and multiply by 100%. There are two important rules to remember when making calculations:

- The sum of all particles must always be equal to 100%. Otherwise, additional rounding should be done, and calculations should be carried out using hundredths.

- There is no fundamental difference in what exactly you are calculating: population size, organization income, manufactured products, balance sheet, debt, active capital, revenue - the calculation methodology will be the same: distributing the part by the total and multiplying by 100% = specific weight.

Subscribe to RSS and you will receive information about site updates to your RSS channel!

Author: gidroadmin

Date of: 2008-12-08

A liquid is a continuous medium that has the property of fluidity, that is, it is capable of unlimitedly changing its shape under the influence of arbitrarily small forces, but unlike a gas, its density changes little when pressure changes.

In aeromechanics, the term “droplet liquid” is used to emphasize the difference between a liquid and a gas; the gas in these cases is called a “compressible liquid”.

Liquids can be ideal or real. Ideal - non-viscous liquids with absolute mobility, i.e. absence of frictional forces and tangential stresses and absolute immutability, and volume under the influence of external forces. Real - viscous liquids that have compressibility, resistance, tensile and shear forces and sufficient mobility, i.e. the presence of frictional forces and tangential stresses.

Real fluids can be Newtonian and non-Newtonian (Bingham). In Newtonian fluids, when one layer of fluid moves relative to another, the magnitude of the shear stress is proportional to the shear rate. At relative rest, these stresses are zero. This pattern was established by Newton in 1686, which is why these liquids (water, oil, gasoline, kerosene, glycerin, etc.) are called Newtonian liquids. Non-Newtonian fluids do not have great mobility and differ from Newtonian fluids by the presence of tangential stresses (internal friction) at rest.

Basic properties of liquids: density, specific gravity, viscosity, compressibility , etc.

Density ρ – mass of liquid per unit volume. For a homogeneous liquid

where m is the mass of liquid in volume V. The units of measurement of ρ in the CGS system are g/cm 3 , in the MKGSS system they are kgf s 2 /m 4 , and in the SI system they are kg/m 3 .

Specific gravity γ – weight of liquid per unit volume:

where G is the weight of the liquid. The units of measurement of γ in the CGS system are dyn/cm 3 , in the MKGSS system – kgf/m 3 , and in the SI system – N/m 3 .

Specific gravity and density are related by the dependence γ=ρ·g, where g is the acceleration of gravity.

Density and specific gravity of some technical fluids.

| Liquid | t, 0 C | ρ, kg/m 3 ; γ, kgf/m 3 | γ, N/m 3 | ρ, kgc s 2 /m 4 |

| Autol 10 | 20 | 920 | 9025 | 93,8 |

| Alcohol (anhydrous) | 20 | 795 | 7799 | 81,0 |

| Ammonia | -34 | 684 | 6710 | 69,7 |

| Aniline | 15 | 1004 | 9849 | 102 |

| Acetone | 15 | 790 | 7750 | 80,5 |

| Petrol | 15 | 680 – 740 | 6671 – 7259 | 69,3 – 75,4 |

| Bitumen | – | 930 – 950 | 9123 – 9320 | 94,8 – 96,8 |

| Distilled water | 4 | 1000 | 9810 | 102 |

| Sea water | 4 | 1020-1030 | 10006-10104 | 104-105 |

| Glycyrin (anhydrous) | 15 | 1270 | 11772 | 129 |

| Tar | 15 | 930-950 | 9123-9320 | 94,8-96,8 |

| Coal tar | 15 | 1200 | 12459 | 122 |

| Kerosene | 15 | 790 – 820 | 7750-8044 | 80,5 – 93,5 |

| Fuel oil | 15 | 890 – 940 | 8731 – 9221 | 90,7 – 95,8 |

| Oil: | ||||

| -vaseline | 20 | 860 – 890 | 8437 – 8731 | 87,7 – 90,7 |

| -industrial 12 | 20 | 876 – 891 | 8594 – 8741 | 89,3 – 90,8 |

| -industrial 20 | 20 | 881 – 901 | 8643 – 8839 | 89,8 – 93,3 |

| -industrial 30 | 20 | 886 – 916 | 8692 – 8986 | 90,3 – 93,4 |

| -industrial 45 and 50 | 20 | 890 – 930 | 8731 – 9123 | 90,7 – 94,8 |

| -industrial 45 and 50 | 20 | 890 – 930 | 8731 – 9123 | 90,7 – 94,8 |

| -castor | 20 | 960 | 9418 | 97,8 |

| -machine | 20 | 898 | 8809 | 91,5 |

| -transformer | 20 | 887 – 896 | 8701 – 8790 | 90,4 – 91,3 |

| -turbine 30 and 32 | 20 | 894 – 904 | 8770 – 8868 | 91,1 – 92,1 |

| Whole milk | 20 | 1029 | 10094 | 103 |

| Natural oil | 15 | 700 – 900 | 6867 – 8829 | 71,4 – 91,7 |

| Beer | 15 | 1040 | 10202 | 106 |

| Mercury | 20 | 13546 | 132886 | 1381 |

| Methyl alcohol | 15 | 810 | 7946 | 82,6 |

| Ethanol | 15-18 | 790 | 7750 | 80,5 |

| Molten cast iron | 17 | 1210 | 11870 | 123 |

Read also: How to measure insulation resistance with a multimeter

Density of water and mercury at different temperatures.

Source: Vilner Ya.M. Reference manual on hydraulics, hydraulic machines and hydraulic drives.

Views: 164260

Comments on this article!!

Comment added by: mqsqt Date: 2011-09-03

Comment added by: Bashtag Date: 2012-10-29

Comment added by: Sanya Date: 2013-11-12

Comment added by: Ir Date: 2014-01-15

Comment added by: ir Date: 2014-04-28

Comment added by: lelik Date: 2014-10-20

Nice way to go

Comment added by: sens Date: 2014-10-23

Thank you very much for the table. It was very useful. ))))

Comment added by: Yuri Date: 2014-12-30

Comment added by: edld Date: 2015-01-28

Comment added by: Vitaly Date: 2018-05-14

Thank you very much for the material

Add your comment

| Similar articles! | |

| Viscosity of liquids | Viscosity of water, milk, gasoline, oil, alcohol | |

| Hydrostatic pressure. Pascal's law. | |

| Bernoulli's equation - the basic equation of hydraulics | |

| Compressibility of liquids | |

| Laminar and turbulent fluid flow regime | |

| The most popular articles on the site! | |

| Conversion of units of measurements. Pressure unit converter | |

| Viscosity of liquids | Viscosity of water, milk, gasoline, oil, alcohol | |

| Density and specific gravity of liquids | Density of water, oil, alcohol, kerosene, gasoline and petroleum | |

| Hydraulic calculation of pipelines | |

| Bernoulli's equation - the basic equation of hydraulics | |

| Laminar and turbulent fluid flow regime | |

| Hydrostatic pressure. Pascal's law. | |

| Thermal expansion of liquids | |

| Compressibility of liquids | |

| History of hydraulics. History of the development of hydraulics. Part 1. From ancient Greece to the mid-18th century. | |

Examples of economic calculations of specific gravity

Let's give a clear example. The director of a wood processing plant wants to calculate the share of sales of a specific type of product - boards. He must know the sales value of a given product and the total volume. For example, a product is a board, beam, slab. Revenue from each type of product is 155 thousand, 30 thousand and 5 thousand rubles. The specific vaginal value is 81.6%, 15.8%, 26%. Consequently, the total revenue is 190 thousand, and the total share is 100%. To calculate the specific gravity of the board, divide 155 thousand by 190 thousand and multiply by 100. We get 816%.

Workers (personnel)

Calculating the proportion of workers is one of the most popular types of calculations when studying a group of workers. The study of qualitative and quantitative indicators of personnel is often used for statistical reporting of companies. Let's try to understand what options exist for calculating the proportion of personnel. The calculation of this indicator has the form of a relative value of the structure. Therefore, it is necessary to use the same formula: divide part of the whole (group of employees) by the whole (total number of employees) and multiply by 100%.

VAT deductions

To determine the share of tax deductions attributable to a certain amount of sales turnover, it is necessary to divide this number by the total amount of turnover and multiply the result by the amount of tax deductions attributable to the total amount of sales turnover. Specific gravity is calculated with an accuracy of at least four decimal places. And the amount of turnover is the number of the tax base and VAT calculated from this tax base, and the amount of decrease (increase) in the tax base.

On balance

The determination of balance sheet liquidity is based on a comparison of assets with liabilities for liabilities. Moreover, the first ones are distributed into groups according to their liquidity and placed in descending order of liquidity. And the latter are grouped in accordance with their maturity dates and arranged in ascending order of maturity. According to the degree of liquidity (the speed of transformation into cash equivalent), the organization’s assets are divided into:

- The most liquid assets (A1) are the entire set of cash items of the organization and short-term investments (securities). This group is calculated as follows: A1 = Money on the company’s balance sheet + Short-term investments.

- Operating assets (A2) – debt to debit, payments of which are expected within a year after the reporting date. Formula: A2 = Short-term accounts receivable.

- Slowly moving assets (A3) are components of the second asset of the balance sheet, including inventories, accounts receivable (with payments that will not be received earlier than in a year), VAT and other defensive assets. To get indicator A3 you need to sum up all the listed assets.

- Hard-to-sell assets (A4) are outside the current assets of the company’s balance sheet.

assets

To determine the specific indicator of any assets of an enterprise, you need to obtain the sum of all its assets. To do this, use the formula: A = B + C + D + E + F + G. Moreover, A is all the assets of the organization, its real estate, C is the total number of deposits, D is all machines and equipment; E – number of securities; F – cash available in the assets of the company; G-patents, company trademarks. Having the amount, you can find the share of a certain type of asset of the organization.

fixed assets

The share of various groups of fixed assets in the total value represents the structure of fixed assets. The share of fixed assets at the beginning of the year is calculated by dividing the value of fixed assets (on the balance sheet of the enterprise at the beginning of the year) by the amount of the balance sheet at the same point in time. First, you need to determine what the company's fixed assets are. This:

- real estate (workshops, industrial architectural and construction facilities, warehouses, laboratories, engineering and construction facilities, including tunnels, roads, overpasses, etc.);

- transmission devices (equipment for transporting gaseous, liquid substances and electricity, for example, gas networks, heating networks)

- machines and equipment (generators, steam engines, transformers, turbines, measuring instruments, various machines, laboratory equipment, computers and much more);

- vehicles (cars, motorcycles, passenger cars for transporting goods, trolleys)

- tools (except special tools and equipment)

- production means, inventory (racks, machines, work tables)

- household equipment (furniture, appliances);

- other fixed assets (museum and library materials).

expenses

When calculating the specific weight of expenses, parts of individual material or other (for example, raw materials) expenses are used. The calculation formula looks like this: expenses are divided by cost and multiplied by 100%. For example, the cost of production consists of the price of raw materials (150,000 rubles), employee salaries (100,000 rubles), energy costs (20,000 rubles) and rent (50,000 rubles). So, the cost is 320,000 rubles. And the share of expenses for salaries is 31% (100 / 320x100%), for raw materials - 47% (150 / 32x100%), for rent - 16% (50 / 320x100%), the balance - 6% falls on electrical costs.

Technology for adjusting plans

Adjusting plans is a mandatory component of the economic activity of any enterprise.

How often and under what circumstances adjustments should be made is decided by management in accordance with enterprise policy. As a rule, deviations of actual indicators from planned ones within +/–10% are considered acceptable and do not require adjustments. In a crisis situation, almost monthly adjustments may be required.

When half of the reporting period - half a year - is already behind us, it is possible to essentially assess the need for adjustments and the degree of compliance between planned and actual indicators.

We will analyze the data for the first half of the year of the main plans of the enterprise (sales plan, financial results plan and unit cost plan) and, if necessary, make adjustments to them.

Sales plan.

This is a forecast document showing the sales volume for all types of products. As a rule, it is formed for the calendar year in the context of each month. Sales forecasts are usually made by marketing department specialists based on the results of an analysis of the market, its conditions and the competitive environment.

The implementation of the sales plan must be constantly monitored, because revenue, profit, etc. depend on sales volume.

Now, due to fluctuations in the supply and demand market, it is problematic to predict sales volumes for the entire year, but without this plan, further financial planning is impossible.

Let's consider the sales plan data for 2022 in comparison with actual sales volumes for the first half of the year (Table 6).

Table 6

Sales plan for the first half of 2022

| Index | Month | Total | |||||||||||

| January | February | March | April | May | June | July | August | September | October | november | December | ||

| Planned number of sales, pcs. (units) | 80 | 80 | 100 | 110 | 120 | 120 | 120 | 120 | 120 | 110 | 100 | 100 | 1280 |

| Actual number of sales, pcs. (units) | 110 | 130 | 160 | 180 | 187 | 190 | — | — | — | — | — | — | 957 |

As you can see, the volume of actual sales exceeds the planned ones by more than 10% (from 30% to 60%). Such deviations cannot be attributed to forecasting errors. In this case, the marketing department (or other authorized division of the enterprise) needs to conduct additional analysis, find out the reasons for the deviation and make adjustments for the second half of 2016.

In this case, the sales volume increased due to the liquidation of a competitor enterprise and the resulting increased demand for similar products of the enterprise. Let's adjust the plan for the second half of 2022. To do this, we will use the average coefficient of deviation of actual indicators from planned ones ((957 - 610) / 610 = 57%).

The adjusted sales plan for the second half of 2022 is presented in table. 7.

Table 7

Adjusted sales plan for the second half of 2017

| Name | Planned number of sales, pcs. (units) | Total | |||||

| July | August | September | October | november | December | ||

| Was | 120 | 120 | 120 | 110 | 100 | 100 | 670 |

| It became | 190 | 190 | 190 | 170 | 157 | 157 | 1054 |

Financial results plan.

Making a profit is one of the main objectives of the financial activities of any commercial organization, therefore special attention is paid to planning financial results.

Earlier, by analyzing the profitability of the enterprise and the data of the interim report on financial results, we found out that one of the main problems of our enterprise is the high cost of production.

At this stage, when half of the reporting period is already behind us, it is possible to adjust costs, namely, implement a cost reduction policy. To do this, we first consider the reported cost calculation for the production of a unit of production (Table 8), which reflects the actual costs of the enterprise and calculates the share of each cost item in the total cost according to data for the first half of 2022.

Table 8

Reporting unit cost calculation

| No. | Costing item | I half of 2022 | Specific gravity, % |

| 1 | Material costs | 35 714,00 | 40,80 % |

| 2 | Labor costs for key production workers | 18 195,00 | 20,79 % |

| 3 | Insurance premiums | 5 458,50 | 6,24 % |

| 4 | General production expenses | 9 735,76 | 11,12 % |

| 5 | General running costs | 18 423,73 | 21,05 % |

| 6 | Production cost | 87 527,00 | 100,00 % |

| 7 | Non-production expenses | 0,00 | 0,00 % |

| 8 | Full cost | 87 527,00 | 100,00 % |

| 9 | Profit | 10 978,00 | x |

| 10 | Price excluding VAT | 98 505,00 | x |

The largest share in the cost structure is the cost of materials (40.80%) - as a rule, this happens at all manufacturing enterprises.

Before you begin to reduce costs, it is necessary to classify costs by priority: from expenses without which the enterprise cannot function normally, to expenses, the absence of which will not significantly affect the activities of the enterprise.

Material costs are classified as significant with a high degree of importance, so we will consider the option of reducing them through negotiations with existing suppliers or changing suppliers to others with more favorable delivery conditions or offering prices that are more acceptable to the enterprise.

For your information

It is not necessary to try to reduce the price for each item of purchased material or component - at this stage it is enough to identify the most expensive material resources and optimize the price of their acquisition.

For example, from the breakdown for the cost item “Materials” we highlight the most expensive type of material - material A, which in the first half of 2022 was purchased from the supplier Alpha LLC at a price of 3,200 rubles per unit. excluding VAT.

To produce a unit of output, 3 units are required. material A (this information can be obtained from approved standards for the consumption of materials or from actual data on the production of similar products). The supplier agrees to provide a discount on material A subject to the purchase of a batch of 3000 units. In this case, the cost of a unit of material will be 2800 rubles. excluding VAT.

We will calculate the need for this material taking into account the remaining stock in the warehouse, paying attention to the shelf life of the material. If it is long-term or open-ended, only the need can be assessed.

So, let's calculate the need. According to the adjusted sales plan for the second half of the year, it is projected to sell 1054 units. products. Therefore, the need for material A will be 3162 units. (1054 x 3). There is a balance of material A in the material warehouse of 518 units.

Thus, in the production of 1054 units. products and purchasing a batch of 3000 units. material at the beginning of the next reporting period there will be a stock of material A in the amount of 356 units. (3000 + 518 – 3162). This is enough to produce another 118 units. products, i.e. a safety stock of materials will be formed for approximately a month.

Now let’s calculate the cost of write-off per unit of production, because there will be two batches of material in the warehouse: one at a price of 3,200 rubles, the second at a price of 2,800 rubles.

At the enterprise, materials are written off at average cost (this information can be obtained from the enterprise's accounting policy):

518 units x 3200 + 3000 units x 2800 = 10,057,600 rubles;

10,057,600.00 / (518 units + 3000 units) = 2858.9 rub.

Taking into account all these calculations, we will form a planned calculation for the second half of 2022 (Table 9).

Table 9

Planned calculation of unit cost of production

| No. | Name of calculation items | FACT I half of 2022 | PLAN II half of 2022 | Changes, +/– |

| 1 | Material costs | 35 714,00 | 34 690,70 | 1023,30 |

| 2 | Labor costs for key production workers | 18 195,00 | 18 195,00 | 0,00 |

| 3 | Insurance premiums | 5458,50 | 5458,50 | 0,00 |

| 4 | General production expenses | 9735,76 | 9735,76 | 0,00 |

| 5 | General running costs | 18 423,73 | 18 423,73 | 0,00 |

| 6 | Production cost | 87 527,00 | 86 503,70 | 1023,30 |

| 7 | Non-production expenses | 0,00 | 0,00 | 0,00 |

| 8 | Full cost | 87 527,00 | 86 503,70 | 1023,30 |

| 9 | Profit | 10 978,00 | 12 001,30 | 1023,30 |

| 10 | Price excluding VAT | 98 505,00 | 98 505,00 | 0,00 |

Thus, by accepting the supplier’s terms, we can reduce the unit cost of production by 1023.3 rubles. Savings with a planned sales volume of 1054 units. products - 1,078,558.2 rubles.

We considered reductions in only one cost item—material costs. Similarly, you can analyze other cost items, classifying them according to the principle of importance.

The greatest effect, as a rule, is achieved by reducing overhead costs. These costs do not directly affect production volume, so reducing them is less painful for the production process. In addition, general production and general business expenses sometimes include absolutely unnecessary and/or grossly inflated expenses.

In general, reducing production costs and optimizing costs is an endless process, so in order to get the best financial result, you must strive to reduce costs or keep them at the same level.

In our case, with an increase in production volume, direct costs (namely, wages and material costs) will increase proportionately. At the same time, you can try to “keep” the total overhead costs at the same level. Then their size per unit of production will decrease as volumes increase.

Information on overhead costs can be found in the reporting calculation for the first half of the year (see Table 8).

So, general production expenses (OPR) per unit of production are 9,735.76 rubles, general economic expenses (OCH) are 18,423.73 rubles.

Knowing the actual volume, we will calculate the total costs for the first half of 2022:

ODA = 9735.76 x 957 = 9,317,122.32 rubles;

OHR = 18,423.73 x 957 = 17,631,509.61 rub.

Now let's calculate overhead costs per unit of production in the second half of the year. To do this, we first find out how to correctly distribute overhead costs between products.

According to the accounting policy of the analyzed enterprise, overhead costs are distributed in proportion to the wage fund (payroll) of the main production workers. Thus, provided that the enterprise produces only the analyzed product with the planned equal level of the wage fund, the distribution will be in equal shares. To calculate, you can simply divide the amount of overhead costs by the planned volume, but we will consider a longer calculation path (this technique is used in the case when an enterprise produces different types of products with different payroll per unit of product).

So, the total payroll of the enterprise will be 19,177,530.00 rubles. (18,195 x 1054), while the share of the payroll of one product in the total payroll of the enterprise will be approximately 0.09488% (18,195 / 19,177,530 x 100%). Based on these data, we calculate the distribution of overhead costs:

ODA = 9,317,122.32 x 0.09488% = RUB 8,839.78;

OHR = 17,631,509.61 x 0.09488% = 16,728.19 rubles.

By reducing overhead costs to optimize costs, you can reduce the cost per unit of production by another 2,591.52 rubles; for the total planned sales volume - by 2,731,462.08 rubles.

Thus, the profit received from the sale of a unit of production will increase from RUB 10,978.00. up to RUB 14,592.83 while maintaining the retail price at RUB 98,505.00. excluding VAT.

Let's adjust the financial results plan taking into account changes in the planned sales volume and reduction in costs for manufacturing a unit of product (Table 10).

Table 10

Planned interim report on financial results for the second half of 2022, thousand rubles.

| Index | Code | FACT for the first half of 2022 | PLAN for the second half of 2022 |

| Revenue | 2110 | 94 269 | 103 824 |

| Cost of sales | 2120 | 83 763 | 88 443 |

| Gross profit (loss) | 2100 | 10 506 | 15 381 |

| Profit (loss) from sales | 2200 | 10 506 | 15 381 |

| Percentage to be paid | 2330 | 332 | 332 |

| other expenses | 2350 | 3947 | 3947 |

| Profit (loss) before tax | 2300 | 6227 | 11 102 |

| Current income tax | 2410 | 1245 | 2220 |

| Net income (loss) | 2400 | 4982 | 8881 |

Based on the received plan, we will calculate the planned profitability indicators:

- total profitability = 11,102 / 103,824 x 100% = 10.69%;

- product profitability = 8881 / 88,443 x 100% = 10%;

- return on sales = 8,881 / 103,824 x 100% = 8.6%.

Conclusion

By reducing the enterprise's production costs while increasing sales volumes in the second half of 2022, it is possible to increase profits by 3,899 thousand rubles.

Profitability indicators increased by an average of 60% compared to the indicators for the first half of the year, which indicates a strengthening of the financial position of the enterprise and an increase in its profitability as a whole.

The minimum minimum value for profitability indicators is 5%. According to data for the first half of 2022, the value of profitability indicators does not greatly exceed the minimum standard. In the second half of the year, thanks to the proposed measures, it was possible to increase the deviations of planned indicators from the minimum standard.

How to automate calculations in Excel?

Specific gravity is determined by the ratio of the weight of matter (P) to the volume it occupies (V). For example, there are 85 students studying at the university, of which 11 passed the exam with “5”. How to calculate their share in an Excel table? You should set the percentage format in the cell with the result, then there will be no need to multiply by 100 - this, like conversion to percentages, happens automatically. We set in one cell (let's say R4C2) the values 85 in another (R4C3) - 11. In the resulting cell you should write the formula = R4C3 / R4C2.